Posts in category 'Home Buying Tips'

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

11

Buying a Home Based on Payments not Interest Rates

|

Over the past few years, we've all gotten used to talking about rates. But buyers? They are thinking about something much simpler: "What is my monthly payment?" They're not thinking about the 10-year Treasury, the Fed commentary, or even the headline rate. It's about the number that hits their checking account every month. And that distinction matters. Interest rates are technical, but payments are about emotion. As a buyer when you hear 6%, you react. But when you hear:

The conversation shifts from fear to clarity. Talking in terms of monthly payments reframes uncertainty into something manageable. A small rate movement can feel dramatic in headlines. But in reality? Sometimes it's the difference of less than a few hundred more per month. That amount may or may not change lifestyle, but when we break it down this way, buyers often realize they are not priced out — they just need context. The strategic advantage When agents and mortgage partners align around payment strategy, buyers can engage faster, their expectations are realistic, increase their confidence , and have improved offers. When buyers aren't chasing rates, they're making informed decisions. What this means for you buyers who paused last year… The first conversation shouldn't be about predictions around the mortgage rate — it should be about payment. Clarity drives action Connect with your loan officer to run real payment scenarios, not hypotheticals. When you understand the numbers you can move forward with confidence. And confident buyers win. |

|---|

9

Buy A Home First or Sell First?

Selling and Buying at the Same Time? Here's What You Need To Know

If you're a homeowner planning to move, you're probably wondering what the process is going to look like and what you should tackle first:

- Is it better to start by finding your next home?

- Or should you sell your current house before you go out looking?

Ultimately, what's right for you depends on a lot of factors. And that's where an agent's experience can really help make your next step clear.

They know your local market, the latest trends, and what's working for other homeowners right now. And they'll be able to make a recommendation based on their expertise and your needs.

But here's a little bit of a sneak peek. In many cases to...

24

Sellers Are coming Back

If you're looking to buy a home, the recent downward trend in mortgage rates is good news because it helps with affordability. But there's another way this benefits you – it may inspire more homeowners to put their houses up for sale.

The Mortgage Rate Lock-In Effect

Over the past year, one factor that's really limited the options for your move is how few homes were on the market. That's because many homeowners chose to delay their plans to sell once mortgage rates went up. An article from Freddie Mac

27

Mortgage Pre Approval Part 2 -Differences

|

|---|

|

|---|

|

|---|

19

What is a Pre Approval

Preapproval, prequalification, automated underwriting, fully underwritten preapproval — all familiar terms, but do you know what they really mean? What impact do they have on your client's loan process or chances for approval? As a seller, what level of assurance does a lender letter offer?

In our two-part series, "All Preapprovals Are Not the Same," we're breaking down these commonly used terms and explaining the advantages and disadvantages of each.

Let's start by clarifying who can make an underwriting decision. In most cases, a lender's designated underwriter will ultimately be making the credit decisions. They rely on the same tools and guidelines that a loan officer does.

AWARD WINNING SERVICES

GLOBAL REACH & HOME INSURANCE

WEBSITE AWARDS

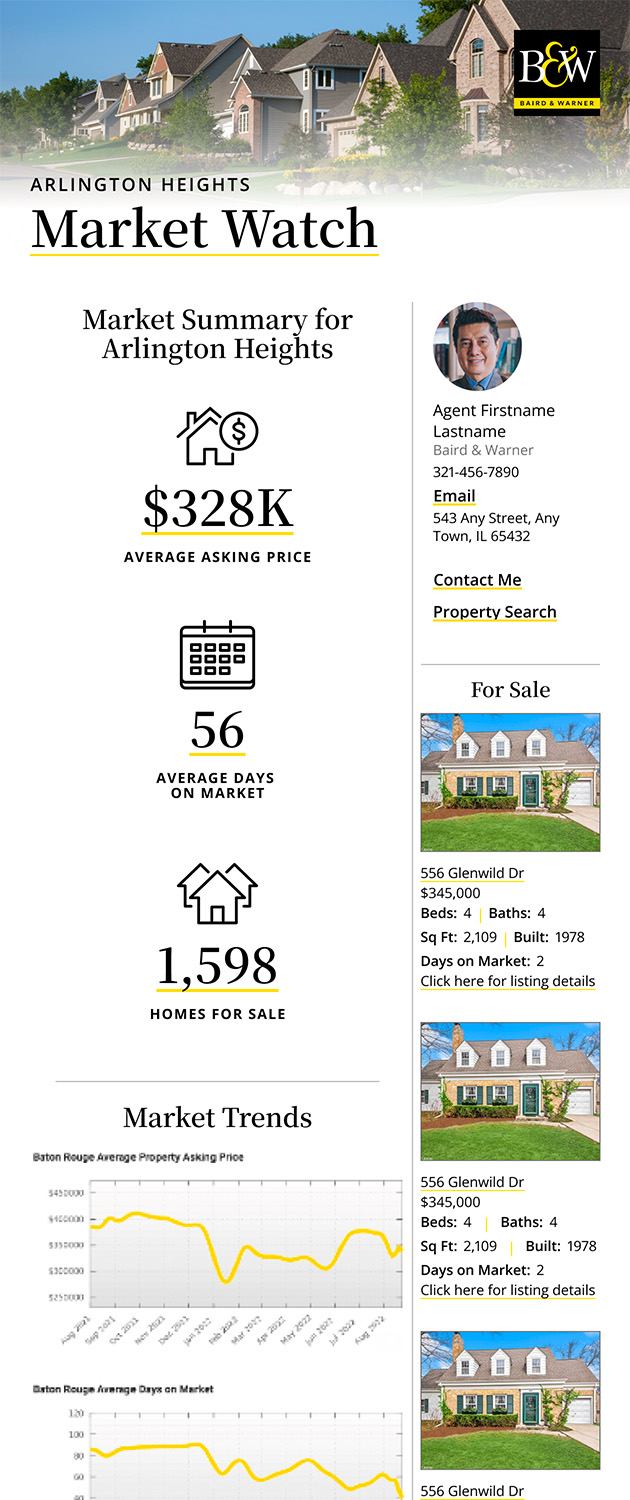

Market Report

Sign up today to stay updated on what’s happening in your local real estate market.