Posts in category 'General Real Estate Updates'

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

11

Buying a Home Based on Payments not Interest Rates

|

Over the past few years, we've all gotten used to talking about rates. But buyers? They are thinking about something much simpler: "What is my monthly payment?" They're not thinking about the 10-year Treasury, the Fed commentary, or even the headline rate. It's about the number that hits their checking account every month. And that distinction matters. Interest rates are technical, but payments are about emotion. As a buyer when you hear 6%, you react. But when you hear:

The conversation shifts from fear to clarity. Talking in terms of monthly payments reframes uncertainty into something manageable. A small rate movement can feel dramatic in headlines. But in reality? Sometimes it's the difference of less than a few hundred more per month. That amount may or may not change lifestyle, but when we break it down this way, buyers often realize they are not priced out — they just need context. The strategic advantage When agents and mortgage partners align around payment strategy, buyers can engage faster, their expectations are realistic, increase their confidence , and have improved offers. When buyers aren't chasing rates, they're making informed decisions. What this means for you buyers who paused last year… The first conversation shouldn't be about predictions around the mortgage rate — it should be about payment. Clarity drives action Connect with your loan officer to run real payment scenarios, not hypotheticals. When you understand the numbers you can move forward with confidence. And confident buyers win. |

|---|

16

Home Prices are Moderating - Not Crashing

Lately, it feels like a lot of people have been asking the same question: "Is the housing market about to crash?"

If you've been scrolling through social media or watching the news, you might have seen some pretty scary headlines yourself. That's why it's no surprise that, according to data from Clever Real Estate, 70% of Americans are worried about a housing crash in 2025.

But before you hit pause on your plans to buy or sell a home, take a deep breath. The truth is: the housing market isn't about to crash – it's just shifting. And that shift actually works in your favor.

Today's Inventory Keeps the Housing Market from Crashing

Mark Fleming, Chief Economist at First American, says:

"There's just generally not enough supp...

11

Mortgage Rates Hit Lowest Point So Far This Year

If you've been holding off on buying a home because of high mortgage rates, you might want to take another look at the market. That's because mortgage rates have been trending down lately – and that gives you a chance to jump back in.

Mortgage rates have been declining for seven straight weeks now, according to data from Freddie Mac. And the average weekly rate is now at the lowest level so far this year (see graph below):

19

Defusing The Zillow Price Estimate

Even if you haven't been selling real estate for long, you've probably spoken to prospects who are convinced that a Zillow price estimate, aka Zestimate, is spot-on. Unfortunately, these can be way off-track and ultimately upsetting, especially to sellers.

To help explain why your listing presentation doesn't mimic the Zillow price, here are some details of how Zillow determines these prices, and why your own market analysis (CMA) is better.

- Zillow pricing uses an algorithm that looks at public property records, tax records, recent home sales, comps, and user-submitted information.

- The algorithm often incorporates older comps into its price determination. Even those that are one year old can result in an off-base price estimate.

- Zestimates often omit renovations, additions, and other changes to properties that affect their value.

- Many attractive Zillow listings are for unavailable homes. Even after a home sale closes, Zillow may r...

25

Should I Buy Now or Wait?

Should you buy a home now or should you wait? That's a question a lot of people have these days. And while what's right for you is going to depend on a lot of different factors, here's something you'll want to consider as you make your decision.

As soon as you buy, you'll start gaining equity. And you'd be surprised how quickly that can add up – even with more moderate home price appreciation.

AWARD WINNING SERVICES

GLOBAL REACH & HOME INSURANCE

WEBSITE AWARDS

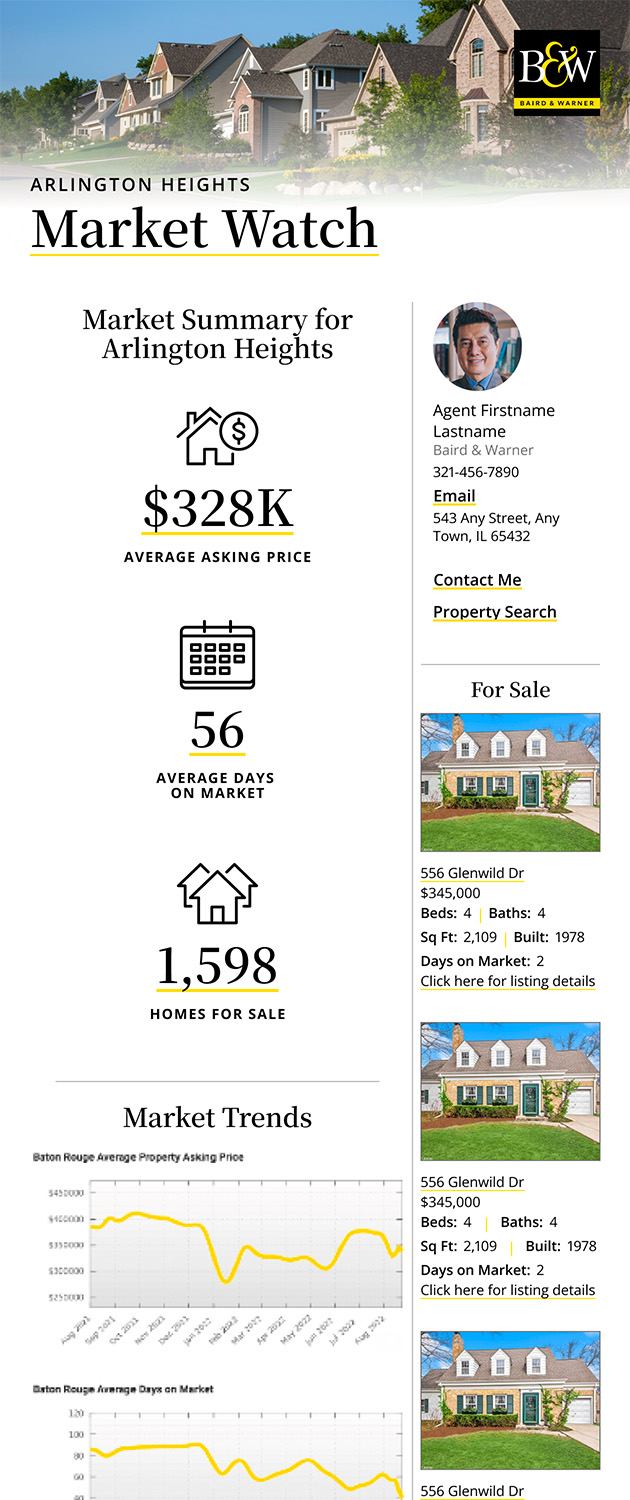

Market Report

Sign up today to stay updated on what’s happening in your local real estate market.